Scenario Analysis Finance

Certainty is a luxury in the world of corporate finance that is seldom available. The amount of revenues changes, interest rates change, supply chains disintegrate, and in a quarter, the market conditions can turn upside down. It is against this backdrop that organisations that simply use a single-point forecast to make their financial planning are working with an incomplete picture. It is this reason why scenario analysis has risen from a niche modelling method to a core discipline in any serious finance function. Being able to construct, analyze and communicate financial situations is one of the most transferable and sought-after skills in corporate finance today.

Corporate financial scenario analysis is, in essence, a systematic approach to the exploration of how financial performance and position of a business can vary under varying sets of assumptions regarding the future. It is not just mere optimism or pessimism. A well-built scenario model compels its authors to determine which of the variables that drive financial results are driving, whether the changes are in sales volumes, commodity prices, foreign exchange rates, or interest costs, and to translate any change in the variables that drive those financial results into specific effects on the income statement, balance sheet, and cash flow statement. This three-statement integration is what can be considered between true financial modelling and back-of-the-envelope thinking.

To professionals in the early and mid years of their careers in the field of finance, the article will be a grounded and practical introduction to the field. It discusses the underlying methodology, the five most important steps in the process, real-life examples based on international corporate environments, the pitfalls that practitioners can most likely fall into, and the lessons that analysts have learnt through their work. It also covers the increasing significance of formal training, the value of courses in financial analysis, to Singaporean-based professionals and the wider Asia-Pacific region. Should you be in need of enhancing your toolkit of analytical tools or you simply want to understand better how the senior management uses financial scenarios to make decisions, this guide is designed to help you get there.

The Role of Scenario Analysis in Corporate Decision-Making

All major financial decisions in a corporation – be they involving capital distribution, debt financing, an acquisition, or a market expansion – are based upon assumptions about the future. The issue is that no one is in the know of what is going to happen in the future. This problem is not solved by scenario analysis, but it re-packages the problem to be fruitfully tackled. Instead of posing the question as to what will happen, it poses the question as to what could happen and whether we are prepared to accept the variety of possibilities. Such a change in framing has far-reaching consequences to the ways in which management teams are planning, boards are overseeing risk and how investors are assessing companies.

Practically, the finance applications of the scenario analysis cover a broad spectrum of corporate scenarios. A manufacturing company, when making a major capital investment, a typical model would typically use a base case to represent the expected demand, a downside case to represent a contraction of demand by fifteen to twenty percent, and an upside case to represent faster-than-expected market penetration. A real estate development company which analyzes a massive project will develop scenarios based on construction prices, financing rates and absorption times. A consumer goods company that is undertaking its annual budget will overlay the scenarios of commodity price volatility as well as currency movement across the markets in which it operates. The output in both instances is not an individual number but a series of outcomes which the management can gauge against their risk appetite and strategic goals.

What sets high-quality scenario analysis finance work apart from basic modelling is the extent to which there is internal consistency of scenarios, and the fact that scenarios are based on real business logic. The ups and downs do not involve simply raising revenues by ten percent on the ups and reducing the revenues by ten percent on the downs. There has to be a plausible scenario as to how the mechanism works: why will revenues go up, and what would that imply about costs, working capital and investment requirements? It is this internal consistency that makes scenarios really decision-useful, and it is what the senior finance leaders (and the financial analysis courses Singapore programmes which train future practitioners) are constantly focused on as the mark of a professional grade of financial work.

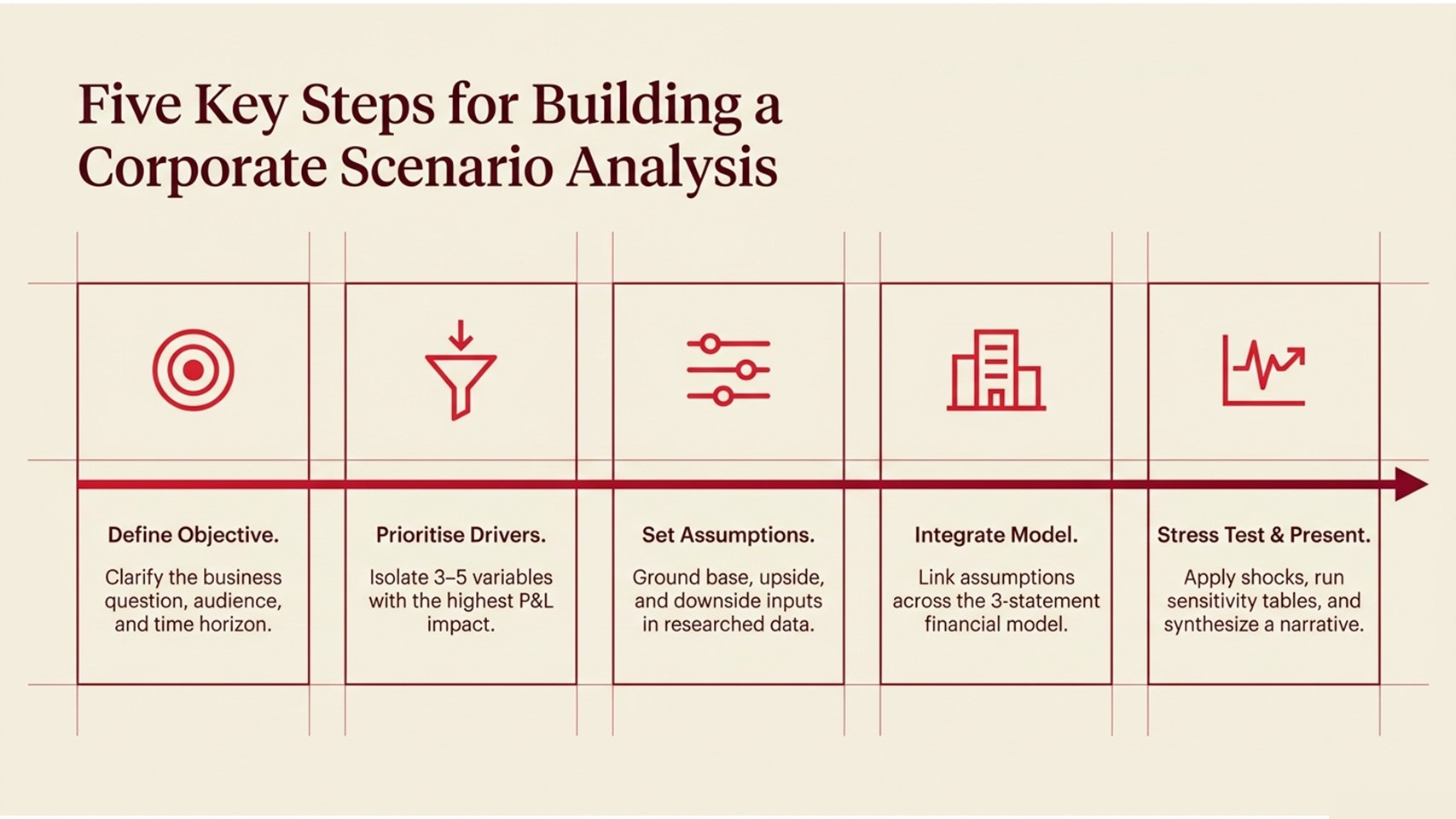

Five Key Steps for Building a Corporate Scenario Analysis

Although details on each scenario model vary by business and industry, the logic behind it remains a similar rationale. The five steps that follow are the standard practice among the corporate finance staffing teams and are a handy guideline to anyone who has stepped into the field of corporate finance for the first time.

Step 1 — Define the Business Question and Objective: Before the analyst can start filling in even a single cell in a spreadsheet, he or she must know what decision he is supposed to support by the scenario analysis. Is it to present a strategic options board presentation? Review of bank covenant? An investor roadshow? The business question decides the time horizon, the detail that is needed, as well as the variables that are most important. A model constructed on behalf of a lender will be focused on the debt serviceability and covenant headroom. A model constructed on behalf of an equity investor will predict returns and growth opportunities in the future.

Step 2 — Identify and Prioritise the Key Drivers: In every business, there are very few variables that, when combined, explain most of the financial variability of the business. The key drivers are the revenue per unit, capacity utilisation, raw material costs, number of people in each position, foreign exchange rate or the cost of borrowing, depending on the sector. Practitioners employ a driver sensitivity analysis to determine which variables influence the EBITDA or free cash flow, and focus their scenario-building effort on them instead of attempting to model all the line items simultaneously.

Step 3 — Set Assumptions Across Scenarios: Once the key drivers have been identified, the analyst makes specific assumptions about the drivers in each scenario – normally a base case, a downside, an upside, with additional cuts of the scenarios added where necessary. The research should be based on assumptions: the range of past historical data, the industry benchmarks, the analysts’ consensus forecasts and the information provided by their operating peers, such as sales heads, procurement teams, and treasury. The assumptions log – a document of the source and rationale of each assumption – is a critical deliverable in its own right since it enables reviewers to question and revise the inputs to the process without having to rebuild the model itself.

Step 4 — Build and Integrate the Three-Statement Model: The assumptions are then transformed into a complete three-statement financial model: the income statement, balance sheet and cash flow statement. Integration implies that when a change in a revenue assumption is made, it automatically flows through to gross profit, operating profit, tax, net income, retained earnings on the balance sheet, and operating cash flow – without any handcrafted changes. This integration constitutes the technical heart of the modelling process, and is the main skill taught in special courses in financial analysis that Singapore-based practitioners depend on.

Step 5 — Stress Test, Sensitise, and Present: The last step is to stress test the outputs of the model, sensitise the model, and present the model outcomes. The synthesis is then presented in a format that can be presented to the senior management or the external stakeholders in a format that can be presented as a presentation.

Outlined below is the five most popular types of scenario applications over the various corporate finance functions, and their common uses:

| Scenario Type | Description | Probability | Typical Use |

| Base Case | Most probable scenario; it is based on the current trends and management projections. | Moderate | Budget planning, valuation |

| Best Case | Wishful thinking; high demand, reduced costs, good rates. | Low | capital raise, M&A pitch. |

| Worst Case | Unfavourable environments: recession, rate surprises, and disruption in the supply. | High | Stress test, covenant examination. |

| Regulatory Shift | Policy change, new compliance costs, and limitations of access to the market. | Variable | Strategic risk management |

| Disruptive Growth | Quick scaling, entering a new market, and acceleration due to technology. | Medium | Presentations to investors, IPO preparation. |

Table 1: Common Scenario Types in Corporate Financial Analysis

The following process flow shows how these five steps are interdependent in modelling a workflow:

| Step 1 | Step 2 | Step 3 | Step 4 | Step 5 | Step 6 |

| Define Objectives | Identify Key Drivers | Set Assumptions | Build the Model | Stress Test Outputs | Present & Decide |

| Define the business question: funding, M&A, budget or review of risk. | Choose 3-5 variables that have the highest revenue or cost implications. | Give values to both Base, Best and Worst cases of each driver. | Associate the assumptions with P&L, balance sheet and cash flow statements. | Shock test – rate increases, FX, and volume declines – test. | Provide clear actions to report findings to the CFO, board, or investors. |

Process Flow 1: Six-Stage Corporate Scenario Model Build Workflow

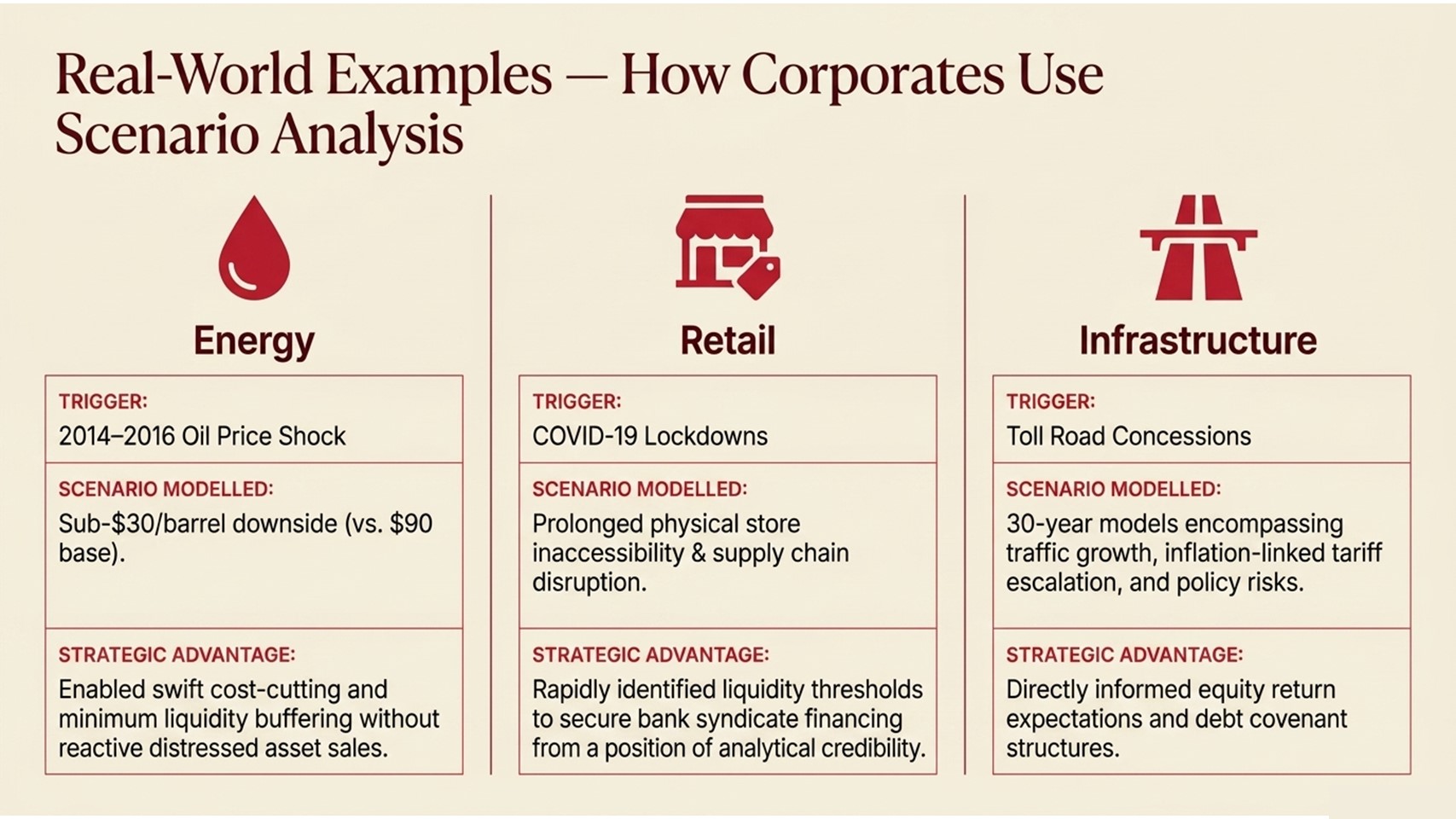

Real-World Examples — How Corporations Use Scenario Analysis

The practical value of structured scenario planning methods becomes clearest when examined through real corporate examples. When the global oil price shock of 2014 to 2016 struck, a number of international energy companies discovered that their single-point capital expenditure plans, based on oil prices above ninety dollars per barrel, failed to endure even a one-point drop in oil prices. Those which had built strong downside scenarios, with well-defined cost-cutting thresholds, sensitivity analysis based on debt covenant sensitivity, and minimum liquidity buffers had been able to respond quickly and systematically. Those that had not had to make reactive expensive adjustments such as emergency equity issues, distressed asset issues and painful renegotiations of covenants.

The issue of international retail groups during the COVID-19 pandemic is a more recent example. One of the big European fashion retailers that had done pre-pandemic structured scenario planning approaches actually had a scenario modelled of physical stores being inaccessible over an extended period, but which was originally conceived as a supply chain disruption scenario and not a pandemic scenario, and operationally equivalent in its financial effects. Due to the existence of the scenario model, the management was able, within days of the lockdown announcements, to run updated figures, identify the point at which liquidity would fall below their threshold, and initiate discussions with their banking syndicate on a platform of analytical credibility. The scenario model failed to stop the loss of revenue – nothing could – but it helped to respond more swiftly and in a more organized way.

Scenario analysis is built into the project finance and infrastructure business environment. A major Australian infrastructure fund that is considering a toll road concession will generally model thirty-year cases that include those assumptions, which are: traffic growth, tariff escalation, which will be linked to inflation, refinancing terms, and government policy risk. It is not just a financial exercise at the analysis level directly informs the equity returns expectations reported to the investors of the pension funds and the form of covenant negotiated with the providers of the debt. The exposure to scenario analysis finance methodology at an early stage in their careers makes junior analysts working in this space more likely to take the rapid track to senior positions than their counterparts who had not been exposed to scenario analysis finance methodology early in their careers.

Challenges in Practice — Lessons Learned from Finance Teams

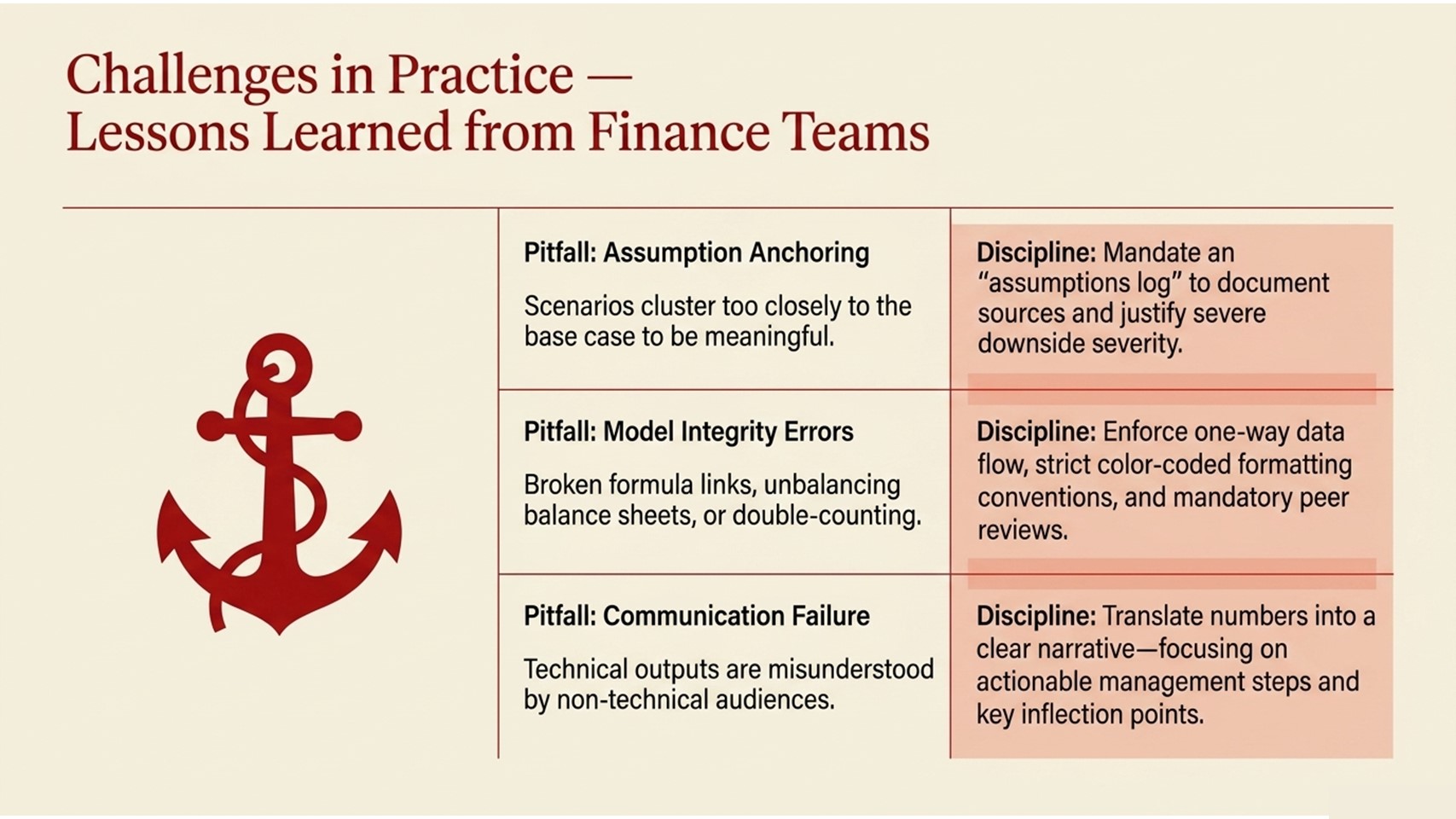

Although it has conceptual simplicity, corporate scenario analysis is nevertheless a challenge that turns out to be quite hard to perform well. One such general challenge is known as by practitioners as assumption anchoring – the tendency to have scenario assumptions clump too closely around the base case, making scenarios that are not meaningfully different relative to each other. This normally occurs when the analysts are not comfortable with presenting the management with some truly pessimistic figures, or the modelling process is motivated by the desired output and not an objective evaluation of what is plausible. The consequence is the setting up of situations that give the semblance of analytical rigour, unaccompanied by the content. In response to this, experienced leaders in the finance industry are putting in place policies that require analysts to record the origin of each assumption and why the downside of each assumption is not more serious.

Another thorny issue is model integrity. With a complex three-statement model with multiple scenario toggles, it is easy to have errors creep in it is hard to write a formula link into a line of code, it is hard to write into a balance sheet what a formula would have linked, and it is hard to write into a cash flow statement what a formula would have connected. Such inaccuracies not only compromise the quality of the analysis but also the legitimacy of the analyst in submitting to senior stakeholders. Structured scenario planning methods address this through discipline: one-way data flow (assumptions feed outputs, not the other way around), colour-coded formatting conventions, and peer review before any scenario output is presented externally.

The third key challenge is communication. A perfect scenario model that has no technical flaws is not of great value when the outputs of such a model can not be explained in a clear manner to a non-technical audience. According to many financial professionals who have undergone financial analysis courses in Singapore or other structured programmes, the communication aspect, that is, learning how to turn numbers into narrative, was as crucial as the technical modelling itself. Being able to stand in front of a CFO or a board committee and explain in plain language why the bad case scenario would create a cash crunch in the third quarter, what the major assumptions that lead to that outcome are, and what management actions could cause those outcomes to occur, is a skill that allows professionals who develop quickly and those who remain technical contributors longer than necessary to stand out.

An overview of the common financial measures in scenario cases to demonstrate the spectrum of outputs a well-organised model ought to generate:

| Key Metric | Base | Best | Worst | Disruptive |

| Revenue Growth (YoY) | +8% | +18% | -5% | +25% |

| EBITDA Margin | 22% | 31% | 11% | 28% |

| Free Cash Flow | +ve | Strong | Negative | High |

| Net Debt / EBITDA | 2.1x | 1.4x | 4.2x | 1.8x |

| Interest Coverage | 4.5x | 7.0x | 1.8x | 5.5x |

Table 2: Illustrative Financial Metric Ranges Across Scenario Cases

The following scenario review cycle describes the way finance teams can manage the end-to-end process, i.e., how finance teams can manage the process of triggering a decision to be made, up to the decision being taken:

| Phase | Activity | Participants | Output |

| Trigger Review | Determine the business event or risk that is in need of scenario modelling. | CFO, FP&A Lead | Scoping document & timeline |

| Model Construction | Prepare or revise a three-statement financial model with scenario switches. | Finance Analysts, Modellers | Integrated scenario model |

| Assumption Validation | Cross-check operation, sales and treasury teams’ assumptions. | Cross-functional team | Assumption log reviewed and signed off. |

| Sensitivity Analysis | Sensitivity tabulate on important variables; find inflection points. | Finance Team | Sensitivity outputs, tornado chart. |

| Decision Briefing | Reports on the results, risks and strategic options in the current scenario to the leadership. | CFO, CEO, Board | Board paper, a record of strategic decisions. |

Process Flow 2: Corporate Scenario Review Cycle — Phase-by-Phase Workflow

Building Scenario Analysis Skills — Training and Professional Development

The professional development market in the Asian Pacific region has grown significantly for those interested in developing or enhancing their corporate scenario analysis skills. The range of financial analysis courses offered by Singapore-based institutions covers both the introductory level of courses based on the Excel spreadsheet program, and those that are more advanced and focus on the integrated three-statement modelling, merger and acquisition valuation, and leveraged buyout analysis. Providers include global institutions which are members of the CFA Institute and ACCA, as well as specialist boutique training firms which only train practitioners in applied financial modelling of corporate and investment finance practitioners.

A key point that professionals opting between training alternatives can note is the difference between conceptual training and applied training, which is a hands-on programme. A course that has taught me the theory of scenario analysis, i.e. the explanation of the concepts without requiring any participants to build a model of the given concepts step by step. The courses in financial analysis that Singapore-based finance professionals reference most often have students build out and defend a complete picture model of a scenario, present their findings to a panel, and receive structured feedback on their technical decisions and their presentation. This realistic method of approach reflects the actual workplace needs and expedites the process of classroom education shifting to workplace input.

In addition to formal classes, at the junior-mid level stage, professionals can hasten their learning by engaging in deliberate practice: volunteering to work on modelling projects in their current organisations, seeking exposure to the entire budget process rather than just one part of it, and reading published financial analysis by investment banks and equity research desks to learn how professional analysts construct and communicate scenarios. To the actively seeking, however, the position in corporate finance, is able to talk fluently about structured scenario planning methods, including the assumptions logic, integration of the financial statements, and the sensitivity analysis layer, is a meaningful differentiator in the hiring process, especially in financial planning and analysis, treasury, and strategy.

Conclusion — Actionable Insights for Finance Professionals

Corporate financial scenario analysis is never a specialized method that only experts in the field know how to effectively use the technique to achieve the desired outcomes. It is the ability to convert uncertainty into a structured range of outcomes and being able to communicate the outcomes clearly and correlate them to actionable management decisions that make finance functions truly strategic partners to the business, as opposed to historical scorekeepers.

The most viable place to begin is to become proficient in the mechanics of an incorporated three-statement model, in the case of professionals in the initial stages of their careers. In the absence of this, the scenario analysis is just a conceptual exercise as opposed to a technical one. Formal training, such as the financial analysis courses Singapore and regionally offered programmes, which focus on model building (hands-on), would offer a structured approach to that technical base. Supplement classroom training with actual on-the-job experience: ask to be included in the budget modelling process, request to see how the finance team at your employer constructs its rolling forecasts and study the sensitivity analysis tables in the board or investor presentations of your employer.

To the professional in the middle ranks who hopes to increase his or her influence, a lesson of the professional long in experience is plain: the analytical product is not of itself the determinant of the influence sought by the practitioner. A scenario analysis finance model built up well, which no one understands or trusts, will not help alter any decision. Just as you invest in the model itself, invest as much time as you can in the communication architecture – in the executive summary, in the visual presentation of the scenarios, in the clear articulation of what can and cannot be controlled by the management. This is where systematic methods of scenario planning contribute their most significant organisational value, which is not based on the spreadsheet, but rather on the quality of the strategic conversation they facilitate.

Lastly, view scenario analysis as an active practice and not a deliverable that occurs every so often. The organisations which cope best with financial uncertainty are those where the finance departments keep their scenario models up to date and continuously updated, and bring scenario thinking into operational debates and decisions, rather than leaving it to formal debate at the board level. The most long-lasting investment that any financial professional can make is in their own ability and in the strength of the organisation in which they work.